For Week Ending September 28, 2024

For Week Ending September 28, 2024

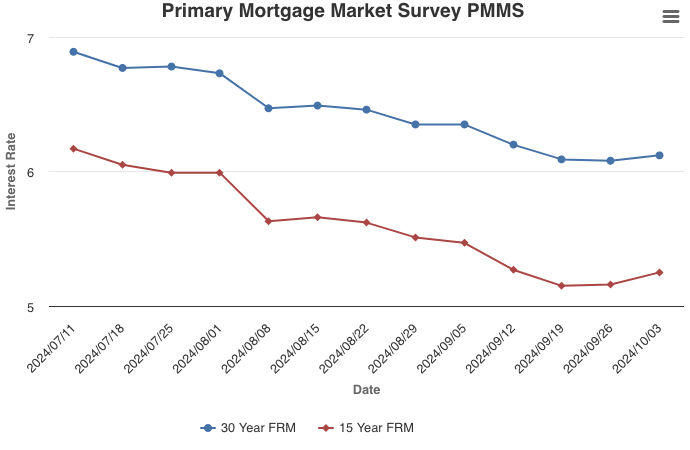

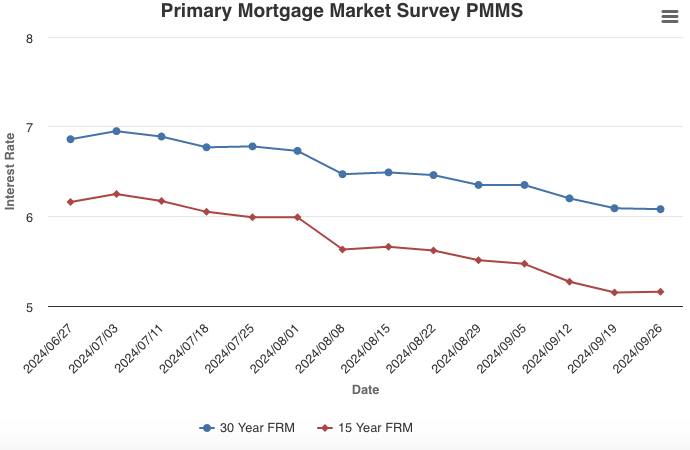

The average rate on a 30-year fixed mortgage dropped to 6.08% the week ending September 26, 2024, the lowest level in two years, according to Freddie Mac. Rates have fallen one and a half percentage points over the past 12 months, and buying power has increased significantly as a result, with Realtor.com reporting the typical homebuyer could afford a home priced $74,000 higher than the October 2023 median sales price for the same monthly payment.

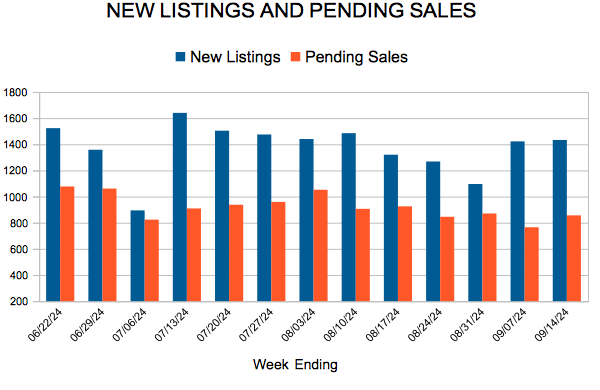

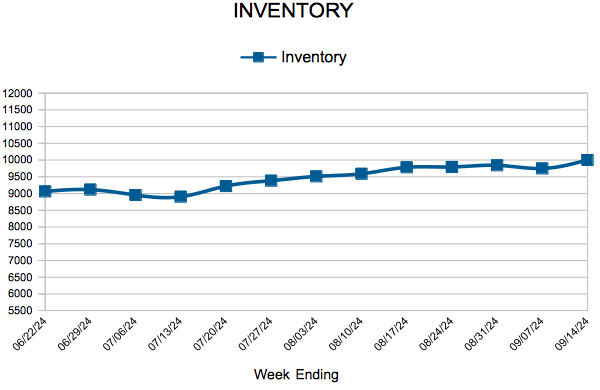

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING SEPTEMBER 28:

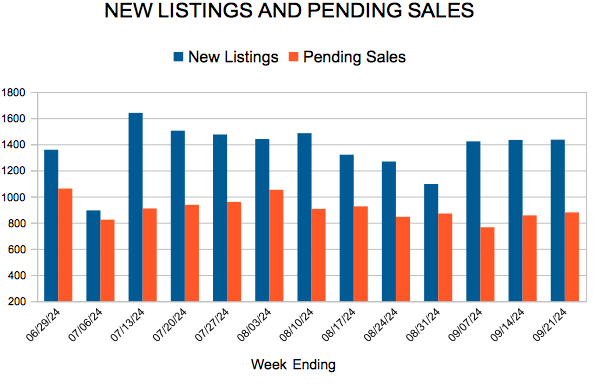

- New Listings increased 11.5% to 1,337

- Pending Sales increased 4.4% to 935

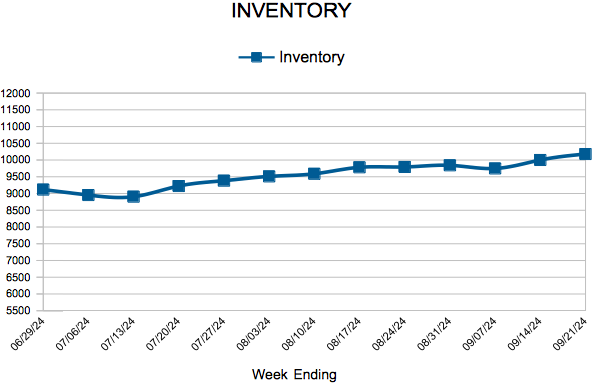

- Inventory increased 12.3% to 10,293

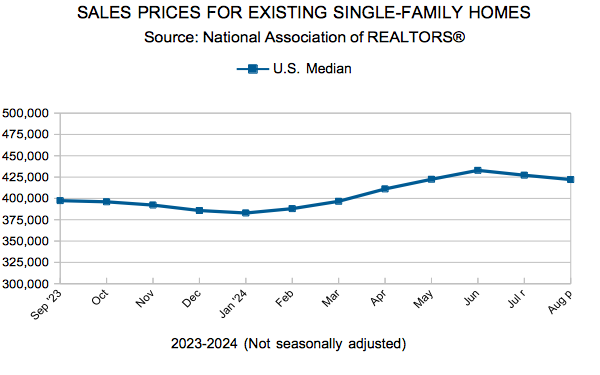

FOR THE MONTH OF AUGUST:

- Median Sales Price increased 2.2% to $388,500

- Days on Market increased 21.2% to 40

- Percent of Original List Price Received decreased 1.3% to 98.7%

- Months Supply of Homes For Sale increased 17.4% to 2.7

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.