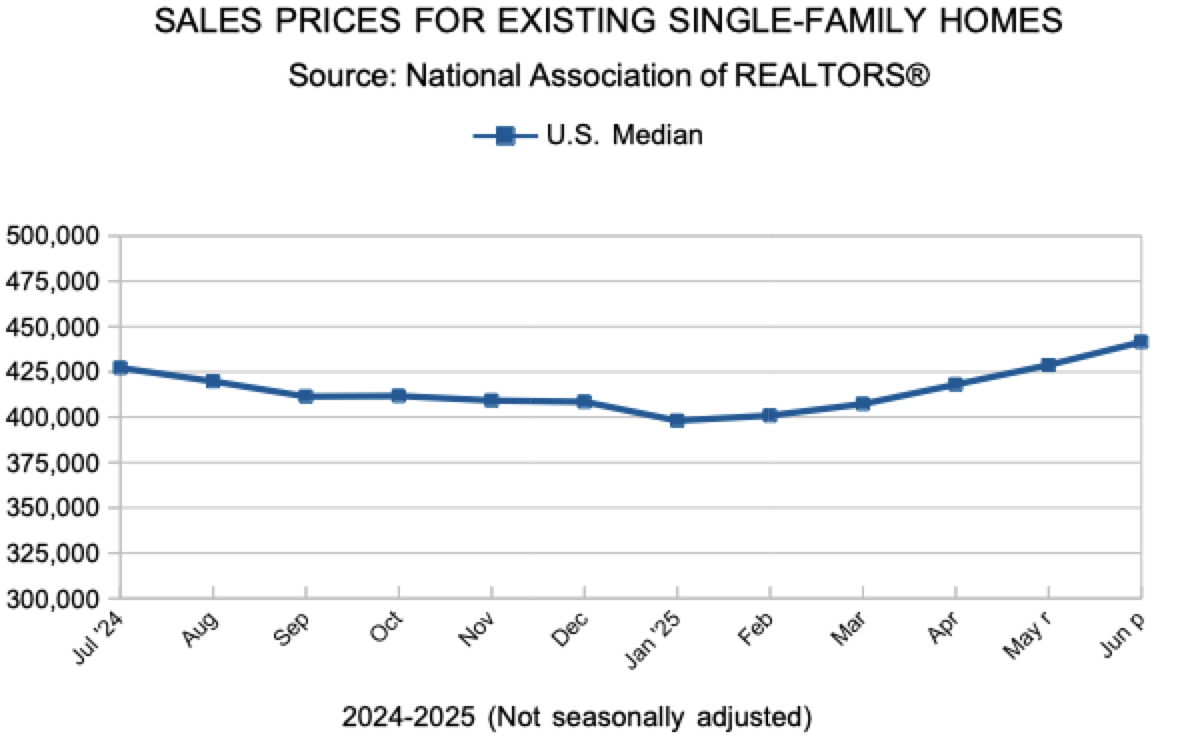

July 24, 2025

This week, the 30-year fixed-rate mortgage essentially remained flat at 6.74%. Overall, the backdrop for the housing market is positive as the economy continues to perform well with solid employment and income growth.

Information provided by Freddie Mac.

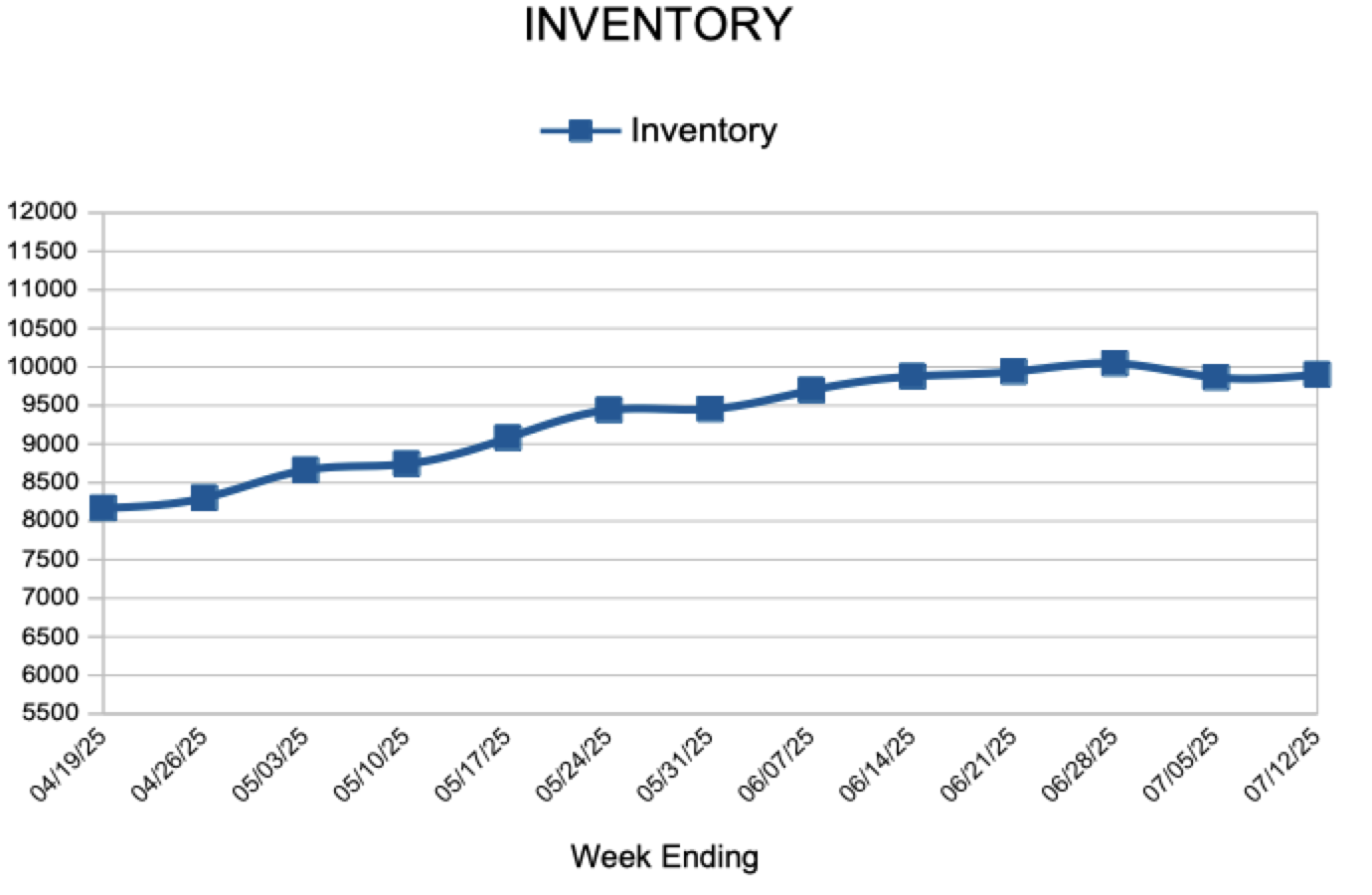

For Week Ending July 12, 2025

For Week Ending July 12, 2025