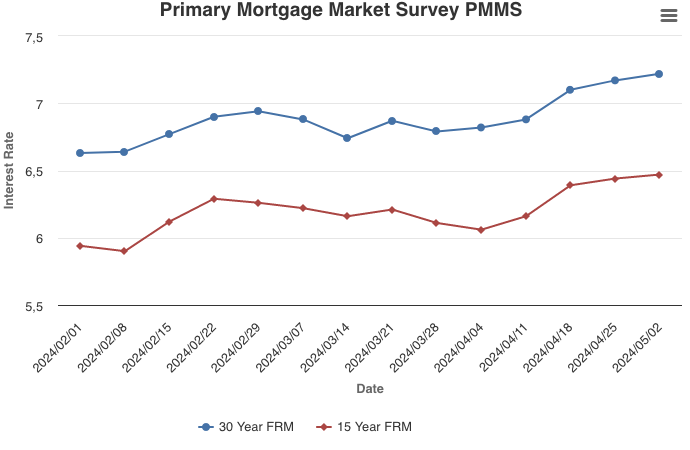

May 2, 2024

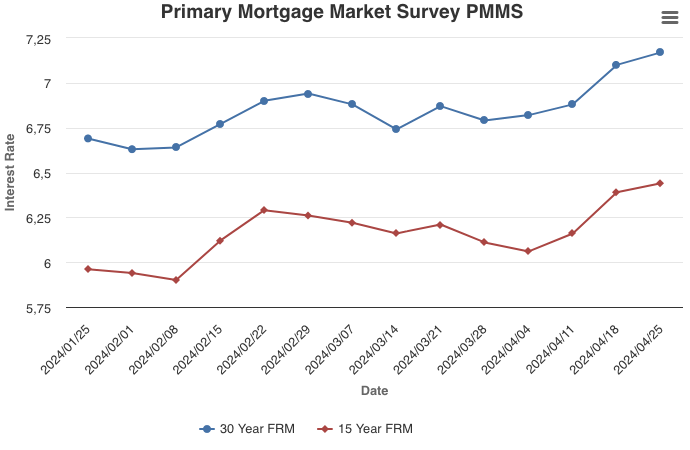

The 30-year fixed-rate mortgage increased for the fifth consecutive week as we enter the heart of Spring Homebuying Season. On average, more than one-third of home sales for the entire year occur between March and June. With two months left of this historically busy period, potential homebuyers will likely not see relief from rising rates anytime soon. However, many seem to have acclimated to these higher rates, as demonstrated by the recently released pending home sales data coming in at the highest level in a year.

Information provided by Freddie Mac.

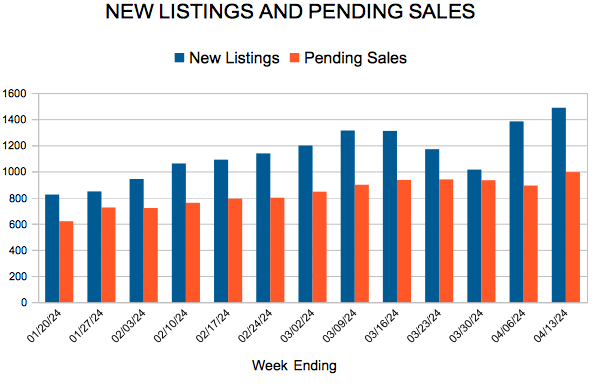

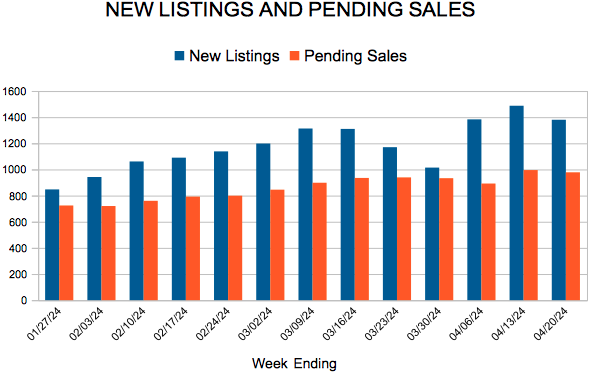

For Week Ending April 20, 2024

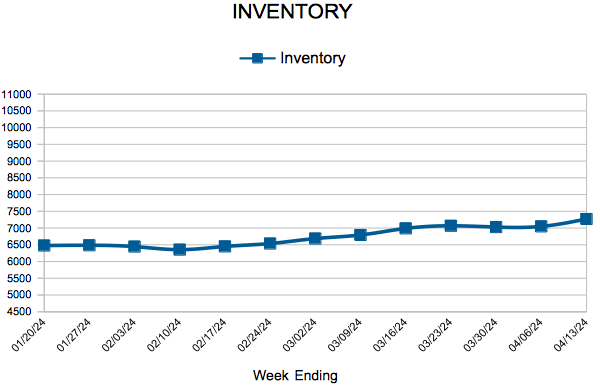

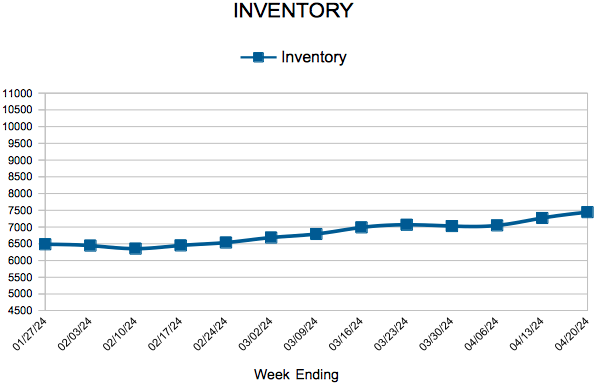

For Week Ending April 20, 2024